Pathways to Sustainable European Energy Systems

The Pathways research programme has, up till now, been carried out in two separate phases, which together span the time period 2006–2013. The main objective of the research programme is to conduct a comprehensive analysis and assessment of the long-term transition of the European energy system towards a significant reduced impact on the climate in Year 2050. This development follows the roadmap towards a competitive, low-carbon economy set out by the European Commission in Year 2011. The focus of the research programme is on the electricity system, and the key topics include: the role of the existing energy infrastructure; defining and analysing scenarios (or pathways) towards Year 2050; and assessing the large-scale integration of renewable electricity. Furthermore, the research presented here considers the entire supply-demand chain of the electricity system, including, to various extent, transmission and distribution.

Main results and conclusions

The results from the first phase of the Pathways research programme have been presented in an earlier book. This executive summary primarily deal with the analyses conducted during the second phase of the Pathways research programme. Nonetheless, as some of the conclusions drawn from the first phase have been reinforced over time, we have retained and adopted these issues in the work presented in this book. Hence, below we give a brief presentation of the most important findings and reflections made during the course of the (second phase of the) Pathways research programme.

It is possible to make deep cuts in carbon emissions until Year 2050, while at the same time maintaining the stability of supply. However, the assessment of the conditions for the different technologies and measures indicate that it is most likely that this will require that all available technologies and measures have to be considered as options towards Year 2050. In theory, while it is of course possible to exclude some technologies based on preferences, considering the large cuts in emissions that are needed, there is a need for compromise rather combativeness when it comes to making technology choices.

Thanks to national support schemes and climate-mitigation policies, the share of renewables in the European electricity generation has increased considerably, and our model analyses emphasise that this trend must continue towards Year 2050 for the pathways that meet the goals set up by the EC. Increased reliance on renewable electricity is, of course, also beneficial from a European security-of-supply perspective. The difference between the scenarios investigated here is related to how large the expansion of renewables will need to become. Thus, the future share of renewable electricity will depend not only on policy, but also on the prospects for other competing CO2-lean supply options, such as natural gas-based electricity generation, Carbon Capture and Storage (CCS), and nuclear power.

CCS represents a response to the threat posed by the large resources of fossil fuels, since it allows fossil fuel-rich countries to combine large cuts in emissions with uninterrupted use of their fossil fuel resources. However, the development of CCS has slowed in recent years and there are few, if any, large CCS demonstration projects in Europe or the US, i.e., the two economies that probably will have to lead the way in developing and demonstrating CCS. The development of CCS is likely to determine the extent of the impact on climate of the continued exploitation of the abundant fossil resources across the world. Moreover, our research shows that in the European context, CCS is essential for the European energy-intensive industry to take its share of the long-term climate-mitigation targets.

From a climate-change perspective, there is clear evidence that fossil fuels are too readily available and abundant around the world. In this book, we lend support to this notion by showing that countries with large resources of fossil fuels have continued to expand their use of fossil fuels at a rate that surpasses their expanded use of renewables. Globally, the richest single source of fossil fuels is coal. That the world may be running out of conventional oil is not the crucial issue, as there are still substantial resources of coal, natural gas, and unconventional reservoirs of hydrocarbons, such as tar sands and oil shale. These large resources are being developed on continuous basis.

Currently (Year 2014), price signals in the European carbon market are too low (4–5 €/tCO2) to stimulate directly investments in carbon-lean technologies. Nonetheless, a cap-and-trade market, in the form of the existing EU Emissions Trading System (EU ETS), is probably the most widely acceptable policy instrument for curbing GHG emissions. If carbon emissions are not priced at a sufficiently high level, it seems highly likely that the use of fossil fuel resources will continue even if the use of renewables is increased through, for example, renewable energy policies. Although renewable policies are important policies for the security of supply and efficiency of the economy, these should be balanced with a stronger climate policy to meet the Year 2050 targets. The scenario analyses described in this book assume that an effective cap-and-trade scheme is in place until Year 2050 to meet the EU climate policy goals. Our research indicates that ETS prices may need to increase to around 100 €/tCO2 by Year 2050 to achieve the required emission reductions.

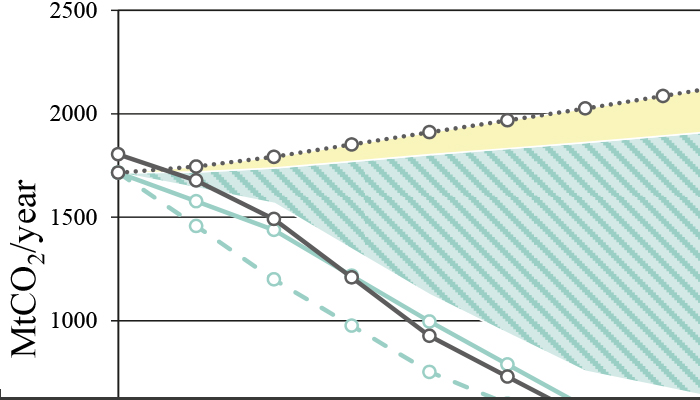

There exists a significant, albeit unexploited, potential to reduce the levels of CO2 emissions from the European electricity supply in the short-term perspective. The model-based calculations reveal that CO2 emissions are reduced by approximately 20% in the electricity sector (or about 5% of the total emissions in the EU) if the EU Emissions Allowance (EUA) price of the EU ETS approaches 40 €/tCO2. This potential for reduction of CO2 emissions is technically feasible in the very short-term perspective, since an increase in the EUA price influences the dispatch of the existing electricity-generating capacity (short-term operation of power plants), whereby efficient gas-fired power plants increase their running times and coal-fired power plants reduce their outputs accordingly. However, given the present oversupply of EUAs, this type of price development appears to be unlikely up to Year 2020. Furthermore, the short-term potential for reduction of CO2 emissions identified here may be jeopardised in the longer term by the currently low level of utilisation of existing, efficient, gas-fired power plants, possibly leading to the permanent closure of these plants.

If fuel and CO2 prices act to favour natural gas (over primarily coal), the potential to reduce CO2 emissions in Europe will be significant, not only in the short-term perspective as mentioned above, but also in a longer time-frame and including new investments in electricity generation based on natural gas. In one of the model calculations, in which we assume a relatively low coal price to gas price ratio (i.e., 2), natural gas consumption in the European power sector increases, with the major increase occurring in the period 2020–2030. Such a development would alleviate the requirement for early deployment of CCS. The resulting increase in gas consumption should not be critical with respect to supply, although it would probably lead to an increased dependency of the EU on imports, which would raise concerns about the security of supply. Therefore, natural gas may offer a bridge towards an almost-zero-carbon-emitting electricity system, also in a medium-term perspective.

An important element to consider regarding the transformation of the energy system is that there is already a system in place, i.e., the present energy infrastructure with installed capacities in place and with associated actors and institutional framework. This comprises a large capital stock with a long turnover time. The databases compiled during our work and the modelling show that existing technologies and fossil fuels will continue to play decisive roles for at least 20–30 years into the future. However, there is a need for substantial investments in new generation capacity while the current plants are phased out, either because they have reached the end of their assumed technical life-time or are incurring too high a cost for emitting CO2. Furthermore, there are legal and social structures, as well as valuable know-how associated with the currently dominant technologies. All these factors will act to preserve the existing system and business models.

Large investments will have to be made towards strengthening, expanding, and upgrading the electricity networks and other infrastructures to accommodate increased levels of wind power and other forms of intermittent electricity generation. Furthermore, a tighter and more flexible linkage between the supply and demand of electricity is likely to require considerable investments in infrastructure related to new technologies and possibilities, such as those provided by advances in information technology. The possible implementation of CCS and the increased use of bioenergy will require an extensive transport infrastructure in the form of a CO2 transportation and storage infrastructure and biomass handling facilities.

The increasing costs for CO2 reduction will increase electricity prices. However, the evolution of electricity prices, in both the wholesale and retail markets, is significantly affected by the ways in which policy instruments are designed and introduced. Generous support for renewable electricity tends to exert downward pressure on the wholesale electricity price, everything else being equal. At the same time, if electricity consumers (rather than taxpayers) are required to fund that support, electricity retail prices may end up at very high levels, as in the case of e.g. Germany for households, commercial enterprises, and smaller industries. In contrast, if policy-making focuses entirely on reducing CO2 emissions, with the consequence that a significant carbon cost emerges, both wholesale and retail electricity prices will be subject to upward pressures.

Based on a detailed GIS-modelling approach, we estimate the realistic potential for onshore wind power in the EU to be approximately 2000–3000 TWh per annum, i.e., 50%–80% of existing gross demand for electricity in the EU. Within this estimate, we have considered possible conflicts with alternative use of land, such as may occur in areas that are densely populated and areas that are subject to environmental protection. Lakes, rivers, and transportation roads are also taken into account in the final estimate. Around half of the identified potential is estimated to be available for exploitation at an overall cost of less than 100 €/MWh. Continued technological developments that reduce specific investment costs or increase the utilisation factor of wind turbines may increase the share of the potential for onshore wind power that is available at relatively low cost. According to our model analyses, not all of the above-mentioned wind power potential of 2000–3000 TWh will be needed, even if the EU meets its long-term climate policy targets towards Year 2050.

Increased shares of variable renewable electricity generation will imply a number of additional challenges being presented to the electricity system. In many aspects, these challenges originate from the natural variability of electricity production from renewable electricity generation, such as from wind and solar power. However, there are several options for accommodating variable electricity generation in the electricity system, for instance:

• Altering the dispatch of thermal power plants, e.g., increasing the utilisation of more flexible and smaller power plants.

• Increasing the flexibility of thermal power plants through investments.

• Considering a geographical allocation of renewable electricity generation installations, so as to dampen variations.

• Improving the transmission and distribution systems.

• Curtailing (i.e., reducing) the production levels of wind and solar power installations, so as to adapt to variations in demand.

• Introducing demand-side management, including load-shifting measures.

• Introducing storage at the supply side, e.g., using fly wheels and pumped hydropower, and at the demand side, e.g., using batteries and active and smart charging strategies for electric vehicles.

These measures are generally associated with additional costs, so-called system integration costs, which also need to be considered in the assessment of large-scale integration of (variable) renewable electricity generation.

A closer look at the different estimates of global biomass resources that have been reported in other studies reveals large variability in the estimates of the supply potentials and availabilities of different bioenergy-resource categories (e.g., 100–1600 EJ by Year 2050). The spread of values may be explained by the fact that many of the determining factors are inherently uncertain, e.g., how society formulates sustainability requirements and policies, and the different regulations as to how land can be used. Biomass from dedicated plantations is generally regarded in the literature as the largest – but also the most uncertain – resource. The size of this resource depends on many factors, not least the demand for animal food products and the land claims associated with meat and dairy production. While many studies commonly adopt food-first principles and introduce restrictions to estimate so-called “sustainable” levels of bioenergy supply, no level of biomass supply comes with a guarantee of sustainability.

Biomass governance (through legislation, best management guidelines or trade standards) is essential, since the deployment of bioenergy involves dealing with a range of environmental, social and economic objectives, which are not always fully compatible with each other. While the emerging bioenergy governance presents many challenges, it is important for ensuring that the rapidly expanding bioenergy industry confers benefits and that the negative effects are avoided or mitigated. As an example, it is presently a matter of some debate as to whether bioenergy from existing forests contributes to climate policy objectives; the discrepant views are partly due to disagreements regarding the assessment methodology and as to whether assessments should consider long-term or short-term effects. A strategy directed towards a more harmonised global approach is considered to be the best option for the governance of bioenergy.

Meeting the climate and energy policy targets of the EU will inevitable have impacts on the demand side. The potential for energy savings on the demand side is known to be large. The challenge lies in creating the policy instruments needed to release a substantial share of that potential. As far as the European building sector is concerned, our research indicates that the final energy demands of that sector could be reduced by approximately 50% (corresponding to the technical potential). Since the European building stock accounts for almost 40% of the total final energy consumption in the EU, the impact of the entire energy supply would be substantial. Furthermore, the demand side may play an important role in the successful integration of large-scale variable renewable electricity generation, such as wind and solar power. To handle the variations in electricity generation, the benefits of being able to control the demand, e.g., by shifting loads in time, become apparent. We have also found that increasing the flexibility of electricity demand, so-called demand response, can improve the economic outcome of small-scale decentralised electricity production, such as photovoltaic (PV) cells.